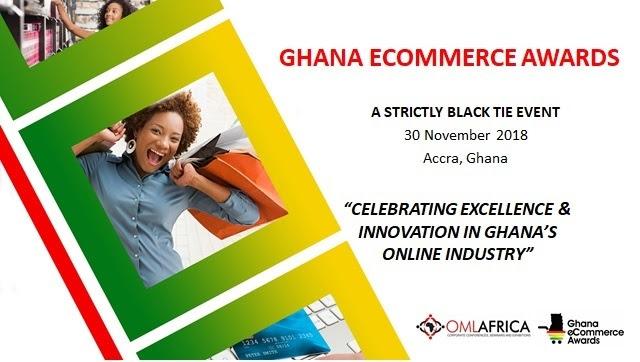

Organizers of the maiden Ghana eCommerce Awards, OML Africa, have announced that nominations’ deadline date of 22 August 2018 will not be extended. Therefore, individuals and companies who fall within the various award categories are encouraged to file their online nominations on the event website www.ghanaecommerceawards.com.

According to a spokesperson of the organizers, “We have already been overwhelmed so far by the number of nominations received for these important awards that are designed to recognize and celebrate excellence and innovation in Ghana’s e-commerce, digital payments, mobile money and fintech ecosystem. The Ghana eCommerce Awards will also boost confidence in doing online transactions and encourage major players to adopt best practice”.

“Our passion and prediction of a boom in e-commerce have remained on course and its only appropriate for OML Africa to organize this landmark event to reward deserving winners in the e-commerce industry which could represent 75 billion dollars across Africa and could account for 10% of Africa’s retail sales by 2025”, he concluded.

After nominations for this year’s awards are collated, an independent panel of 5 selected judges comprising Professor Atuahene-Gima (Founder, Noble International Business School); Dr Kajsa Hallberg-Adu (lecturer, Ashesi University and Founder, BloggingGhana); Stephen Nana-Osei Boadi (Chief Digital Enabler, Enable Growth Africa); Berthold Gadagbui (Head, Mobile Banking, Ecobank) and Anita Wiafe-Asinor (Owner, Delilah Secrets & savvy online shopper) will choose finalists for each category based on a pre-selection criteria.

Some award categories are Best Online Retailer, Best Fintech Company, Best Fintech Innovation, Best Small Independent Retailer, Best Sin-Store Initiative, Best Online Retail Marketing, Best Site Optimization & Design, Best Mobile eCommerce and Best Online Real Estate Site.

Others are Best Social Media Campaign, Best Omni Channel Customer Service, Best Delivery/Courier Service eCommerce, Best Female eCommerce Entrepreneur, Best eCommerce Banking App, Best eCommerce Payment Company and Best eCommerce Innovation.

The rest are Best Internet Service Provider, Best Innovation in eCommerce (Payments), Best Online Food Delivery Platform, Best Online Hotel Site, Best Online Betting Site, Best Bitcoin Company and Best Online Retailer (Electronics).

These prestigious awards for Ghana’s online business industry are also to boost the ever-increasing trend of consumers going online to shop and doing so, more safely and conveniently. It will also augment government’s efforts in making Ghana a cashless society and contribute immensely to achieving “The Ghana beyond Aid” Agenda as e-commerce is rapidly becoming an increasing contributor to the GDPs of African countries.

The organizers, OML Africa, have the pedigree as a pioneer in organizing high-quality exhibitions and conference in Ghana’s e-commerce space, having held four Ghana eCommerce Expositions, which have been the hub for the online business community since 2013!